(Bloomberg) — The bond market is growing less convinced by the day that the Federal Reserve will embark on two further interest-rate cuts this year.

Most Read from Bloomberg

Traders are pricing in roughly 20% odds that the Fed holds rates steady in either November or December. This time last week, even after Friday’s blockbuster jobs report, swaps still implied more than 50 basis points of cuts by year-end, likely via consecutive cuts.

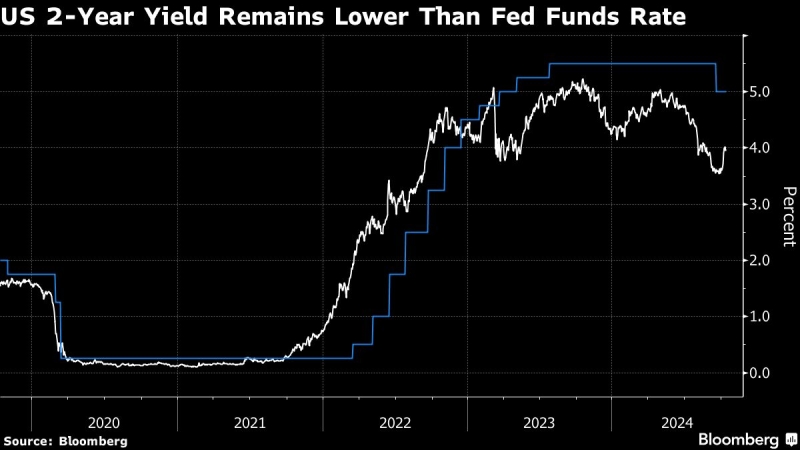

Treasuries have slumped this week as a result. A Bloomberg gauge of US bonds is poised for a fourth-straight week of declines — its worst streak since April. Yields on 10-year notes are back above 4%, and the 30-year bond’s yield touched 4.42%, the highest level since July 30.

The shift reflects a slew of mixed reports on the US economy that have failed to make the case for significantly looser monetary policy. While the Fed’s so-called dot plot showed officials’ median rate expectations project two further cuts this year, nine of 19 officials saw only one reduction at most.

That division among the hawks and doves at the Fed has been on display this week. A handful of Fed officials, including New York Fed President John Williams, mostly shrugged off higher-than-expected consumer inflation gauges released Thursday and signaled they support continued rate reductions. Atlanta Fed President Raphael Bostic, however, said he would consider a pause in rate cuts, and Dallas Fed President Lorie Logan reiterated Friday that interest rates should move at a slow pace to a more normal level.

“The market is less sure about what happens in upcoming FOMC meetings, but more confident — judging by a near-50-basis-point rise in 10-year yields since mid-September, that a ‘hard landing’ is going to be avoided,” Societe Generale SA’s Kit Juckes wrote in a note. That suggests a view that “‘no-landing’ is as likely as a soft landing, bringing with it concern that if fiscal restraint isn’t forthcoming, upside inflation risks may re-emerge.”

Thursday’s September consumer price index report reinforced signs of an uptick in wage pressures seen in last week’s payrolls data. Wholesale prices data released Friday were more benign overall.

Some investors say the selloff provides buying opportunities because the Fed remains on the course of policy easing, even if the pace of rate reduction remains uncertain.

“We do see there’s a bit of value in buying, not necessarily in the long end, but rather in one- to five-year” sectors, said Leslie Falconio, head of US taxable fixed income strategy in UBS Asset Management’s chief investment office, on Bloomberg Television. “They are still on a path of normalizing” interest rates, she said.

Activity in derivatives markets shows investors hedging for fewer rate cuts than currently expected. Demand for options referencing the Secured Overnight Financing Rate has focused on contracts that target one additional rate cut this year. In the futures market, there’s been a wave of liquidations of bets on bond gains.

Friday’s Treasury options flows included several notable bearish wagers that helped steepen the yield curve. A purchase of December puts on 10-year notes targeted a yield increase to around 4.5% by their Nov. 22 expiration date, while a couple of large block trades of December puts on the Bond contract look for a yield increase to roughly 4.75% by the same date.

The impending US presidential election is also on investors’ mind. Ella Hoxha, head of fixed income at Newton Investment Management, a UK-based asset manager, said she’s cut exposure to long-dated US Treasuries to reduce the risk exposure in the run-up to the Nov. 5 election.

“It makes sense here to have lower levels of risk, particularly given that we have quite a bit of event risks ahead of us over the next several weeks,” Hoxha said in an interview with Bloomberg Television.

(Adds option market activity and Fed officials’ comments.)

Most Read from Bloomberg Businessweek

©2024 Bloomberg L.P.