(Bloomberg) — The Federal Reserve’s preferred price metric and a snapshot of consumer demand are seen corroborating both the central bank’s aggressive interest-rate cut and Chair Jerome Powell’s view that the economy remains strong.

Most Read from Bloomberg

Economists see the personal consumption expenditures price index rising just 0.1% in August for the second time in three months. The inflation gauge probably climbed 2.3% from a year earlier, the smallest annual gain since early 2021 and a shade higher than the central bank’s 2% goal.

The slowdown in inflation from a year ago reflects falling energy and weaker food prices, along with moderating core costs. The PCE price gauge excluding food and fuel probably rose 0.2% for a third month, economists expect government data to show Friday.

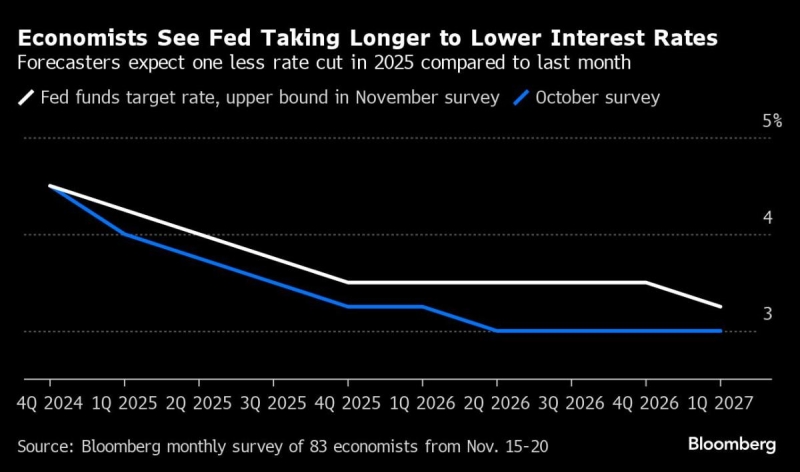

The step-down in inflationary pressures from earlier this year provided Fed policymakers with enough confidence to lower rates on Sept. 18 by a half percentage point. The cut was the first in more than four years, and represented a pivot in the central bank’s policy toward averting a deterioration in the job market.

Investors will parse remarks from a large number of Fed officials in the coming week. Governors Michelle Bowman, Adriana Kugler and Lisa Cook, along with regional presidents Raphael Bostic and Austan Goolsbee, are among those set to appear at various events.

The August inflation figures will be accompanied by data on personal spending and income, and economists project another solid advance in household outlays. Sustained consumer spending growth helps raise the chances that the economy will continue expanding.

Other economic data include August new-home sales, second-quarter gross domestic product along with annual GDP revisions back to 2019, weekly jobless claims, and August orders for durable goods.

What Bloomberg Economics Says:

“In our view, the Fed’s jumbo cut increases the chance of a soft landing, but by no means ensures it. Our baseline is still for the unemployment rate to reach 4.5% before the end of 2024, before rising to 5% next year.”

— Anna Wong, Stuart Paul, Eliza Winger, Estelle Ou and Chris G. Collins, economists. For full analysis, click here

In Canada, GDP data for July and a flash estimate for August are expected to show weak growth in the third quarter, likely below the Bank of Canada’s forecast of 2.8% annualized expansion. Meanwhile, the central bank’s governor, Tiff Macklem, will speak at a banking conference in Toronto.

Elsewhere, the OECD will reveal new economic forecasts on Wednesday, central banks in Switzerland and Sweden may deliver rate cuts, and their Australian counterpart is anticipated to stay on hold.

Click here for what happened in the past week and below is our wrap of what’s coming up in the global economy.

-

For more, read Bloomberg Economics’ full Week Ahead for the US

Asia

The Reserve Bank of Australia is expected to keep its cash rate target unchanged at 4.35% when the board meets on Tuesday, with the focus likely to fall on whether Governor Michele Bullock retains her hawkish tone after solid labor figures prompted traders to pare bets on a December rate cut.

Bloomberg Economics still sees a path to potential RBA easing in the fourth quarter. Authorities will have to wait until Wednesday to see if Australian inflation cooled for a third month in August.

Other nations releasing inflation updates include Malaysia and Singapore, where price growth is forecast to have slowed in August.

Japan gets fresh inflation data with the release Friday of Tokyo consumer prices, which are expected to have risen at a pace exceeding the Bank of Japan’s 2% target in September.

Purchasing manager indexes for September are due from Australia and India on Monday and from Japan a day later.

In China, the 1-year medium term lending facility rate is expected to be held unchanged at 2.3%, and data Friday will show whether industrial profit growth maintained momentum in August after rising at the fastest clip in five months in July.

Trade statistics are due from South Korea, Thailand and Hong Kong.

-

For more, read Bloomberg Economics’ full Week Ahead for Asia

Europe, Middle East, Africa

Four central bank decisions are scheduled in Europe, where investors may question the appetite of policymakers to follow in the footsteps of the Fed with a half-point cut.

That’s certainly the case with the Swiss National Bank on Thursday. While a majority of economists foresee a quarter-point move, observers do reckon the US reduction has increased the chances of a step of the same size as officials confront the persistent strength of the franc. This is the final meeting for President Thomas Jordan, whose term concludes at the end of the month.

The previous day, Sweden’s Riksbank is expected to lower borrowing costs by a quarter point for the third time this year, taking the rate to 3.25%, and to outline a path to additional cuts.

The current guidance is for two or three more moves in 2024 — including on Wednesday. Policymakers talked about a half-point cut at last month’s meeting, and while that discussion could come up again, most economists believe the central bank would more likely wait until November to do a bigger move.

In Eastern Europe, meanwhile, both the Hungarian central bank on Tuesday and its Czech counterpart on Thursday are expected to deliver quarter-point reductions.

In the euro zone and the UK, an initial look at purchasing managers indexes for September will be released on Monday, signaling the state of private-sector activity at the end of the third quarter.

With Germany’s weakness a focal point for investors, the Ifo business confidence gauge will be a highlight on Tuesday, the same day Bundesbank President Joachim Nagel is due to speak on the economy. New forecasts from the country’s economic institutes are scheduled for Thursday.

Readings of French and Spanish inflation for September will draw attention on Friday, hinting at the overall outcome for the region due the following week. Economists predict both countries’ readings will drop below 2%.

Aside from Nagel, more than half a dozen euro-zone policymakers are scheduled to speak, including European Central Bank President Christine Lagarde, chief economist Philip Lane, and Spain’s new central bank chief Jose Luis Escriva.

Across the African continent, various central bank decisions are also scheduled:

-

Nigerian officials on Tuesday will likely pause a tightening cycle that’s lifted the rate to 26.75% from 11.5% in just over two years. They’ll be encouraged by inflation cooling to a six-month low as they weigh the impact of floods in the country and a steep increase in gasoline costs on price growth.

-

Morocco’s central bank will probably hold its rate at 2.75% to allow time for June’s surprise cut to seep through the domestic market. The kingdom needs low rates to facilitate investment and contain unemployment. It has massive investment plans for reconstruction of earthquake-hit areas and infrastructure ahead of the FIFA World Cup in 2030.

-

In southern Africa, officials in Lesotho may diverge from South Africa’s rate cut and leave borrowing costs at 7.75%, as inflation stays elevated. While Lesotho tends to mirror the policy of its neighbor, its key rate is already 25 basis points lower.

Elsewhere, Zambia’s Finance Minister Situmbeko Musokotwane will on Friday announce plans to help the economy bounce back from one of the toughest years it’s faced this century when he unveils his 2025 budget for Africa’s second largest copper producer.

-

For more, read Bloomberg Economics’ full Week Ahead for EMEA

Latin America

Brazil watchers will have a lot to digest, with minutes of the central bank’s September rate meeting and a quarterly inflation report taking center stage.

The former may provide a more detailed policy road-map after a quarter-point hike on Sept. 18, to 10.75%, while the latter updates all manner of economic estimates and scenarios. Look for the BCB to mark up forecasts for inflation, the key rate, and GDP growth.

Rounding out the week for Latin America’s biggest economy, jobs data will likely show Brazil’s labor market remains at historically tight levels while mid-month inflation may have stalled near the top of the central bank’s target range.

Argentina is slated to post GDP-proxy readings for July, which may build support for the view that the economy is past its 2024 nadir and is beginning a second-half recovery.

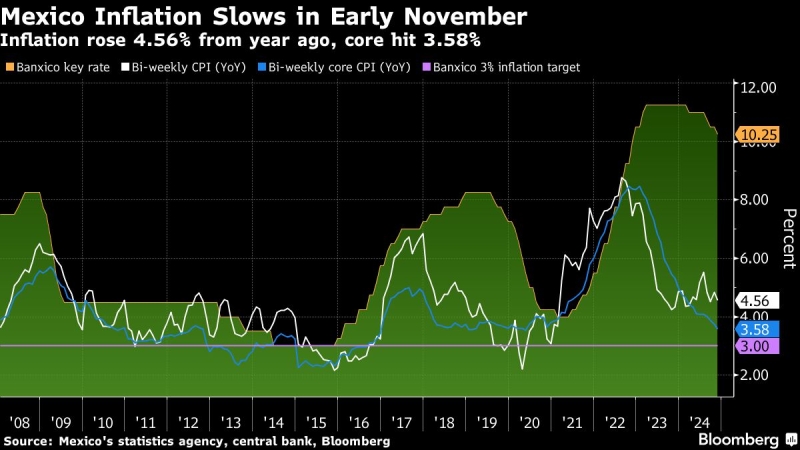

In Mexico, downshifting domestic demand may see another set of soft retail sales prints — on the heels of June’s negative annual and monthly readings — while mid-month inflation data aren’t likely to provide policymakers with a slam dunk cause to cut or hold when Banxico meets a few days later.

The early consensus expects a quarter-point cut to 10.5%, though some analysts see a possible half-point reduction to stay on pace with the Fed.

-

For more, read Bloomberg Economics’ full Week Ahead for Latin America

–With assistance from Brian Fowler, Robert Jameson, Niclas Rolander, Monique Vanek, Piotr Skolimowski, Matthew Hill and Souhail Karam.

Most Read from Bloomberg Businessweek

©2024 Bloomberg L.P.